Home insurance costs are rising in 2026, and South Florida homeowners and buyers are feeling the impact more than most. From higher rebuilding costs to ongoing hurricane risk, insurance premiums across coastal markets like Fort Lauderdale, Miami, and West Palm Beach remain elevated. Whether you already own a home or are planning to buy, understanding what’s driving these increases (and learning smart ways to save) can help you make more informed decisions and protect your long-term investment.

Quick Read

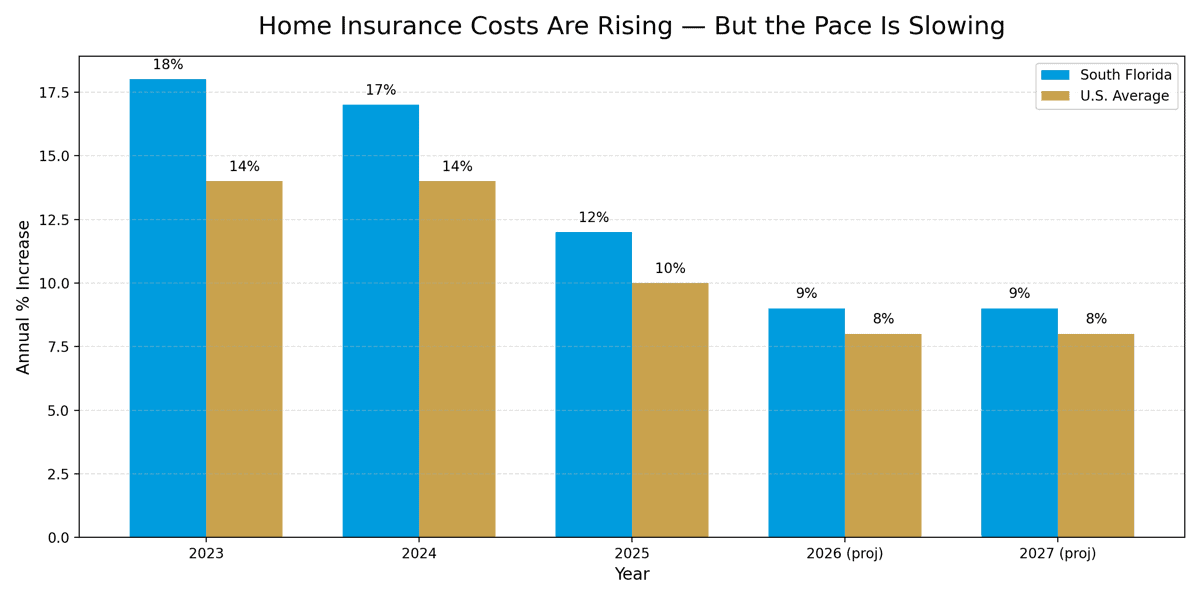

- Home insurance costs are rising in 2026, with South Florida hit hardest

- Florida premiums are up 30–40% since 2022, despite slowing increases

- Both homeowners and buyers should plan for insurance as a long-term cost

- Smart planning and home upgrades can help reduce premiums

Homeowners insurance helps protect your property from damage caused by storms, fire, theft, and liability claims. But as insurers face higher claim payouts and rising rebuilding costs, premiums are increasing nationwide. In coastal markets like Fort Lauderdale, Miami, and West Palm Beach, these trends are amplified by hurricane exposure, flood risk, and stricter underwriting standards.

Why Insurance Costs Are Increasing

Several overlapping factors are contributing to higher insurance premiums:

-

Severe weather and climate risk: Stronger hurricanes and more frequent storm-related claims raise insurer losses.

-

Rising construction costs: Higher labor and material prices increase the cost to repair or rebuild homes.

-

Reinsurance costs: Insurance companies purchase their own coverage, and those costs have risen significantly in recent years.

-

Reduced market competition: Some insurers have limited coverage or exited high-risk markets, including parts of Florida.

In Florida specifically, premiums have increased significantly over the past few years, with some reports showing cumulative jumps of 30–40% since 2022, even as the pace of increases appears to be slowing in 2025 and 2026. Despite signs of stabilization, Florida remains one of the most expensive states in the country for homeowners insurance — particularly in coastal and waterfront areas.

What This Means for Homeowners

For current homeowners, insurance is not a fixed expense. Premiums can change annually based on market conditions, replacement costs, and property-specific risk factors — even if you’ve never filed a claim.

Tips for homeowners:

-

Review your policy annually to ensure coverage and deductibles still make sense

-

Ask about discounts for impact-resistant windows, newer roofs, or updated systems

-

Compare quotes periodically instead of automatically renewing

-

Keep up with maintenance to reduce inspection issues and potential claims

What Buyers Should Plan For

For buyers, homeowners insurance should be factored into affordability just like taxes and mortgage payments. Premiums in South Florida can vary widely based on roof age, elevation, construction type, and proximity to the ocean or Intracoastal Waterway.

Tips for buyers:

-

Request insurance estimates early in the buying process

-

Understand how wind mitigation and roof age affect pricing

-

Budget for long-term insurance costs, not just year one

-

Work with local professionals who understand South Florida insurance dynamics

Bottom Line

Rising home insurance costs are a reality for both homeowners and buyers in South Florida. While increases may be slowing, premiums remain elevated. Staying informed and planning ahead can help protect both your home and your finances.

If you’re a homeowner or buyer navigating today’s South Florida luxury real estate market, working with a local expert can help you plan ahead, from understanding true ownership costs to choosing a home that aligns with both your lifestyle and budget. Let’s connect!